The study of society and the way individuals interact within it.

Examples include sociology, political science, psychology, anthropology, history, and (of course) economics.

Needs

Something we MUST have in order to survive (e.g. water, food, housing)

Wants

Something we desire (e.g., pens, computers, automobiles)

We have unlimited wants and limited resources

Economics

The study of rationing systems; of how society employs its finite resources in the attempt to satisfy infinite wants

Microeconomics

The study of individual economic units such as households and firms

Macroeconomics

The study of the economy as a whole (e.g., a country, inflation, unemployment)

Market

A market is a medium that allows buyers and sellers of a specific good or service to interact in order to facilitate an exchange.

Economic growth

An increase in real GDP or an increase in the quantity of resources

Gross Domestic Product (GDP) is the most commonly used measure for the size of an economy

See PPF diagram at right

Economic development

A qualitative measure of a country's standard of living which takes into account numerous factors such as education and health

The Human Development Index is normally used to measure a country's economic development

Sustainable development

The rate at which a country can develop without compromising the needs of future generations

Positive and Normative Concepts

Positive: Based on testable theories (e.g., a hike in interest rates leads to a fall in aggregate demand can be proven using data)

Positive economics is based on theories which can be tested by looking at past data

Positive statements concern what is, was or will be: assertions about the world

Normative: Based on opinion/norms

Uses words such as "should" (i.e., the government should make fixing unemployment its number one priority)

Normative economics is based on opinion

Normative statements often include words such as ‘should’ or ought to’ and involve value judgements about what is good and what is bad

Normative statements are not testable: 'ought we to be more concerned about unemployment than about inflation?'

In democracies normative statements are often settled by voting

Ceteris Paribus

Latin for all other things being equal

Since Economics is basically the study of society, we have to understand that there are thousands of variables present, and to control each one of these variables is downright impossible

Thus we make everything else "ceteris paribus" in order to see the effect of one aspect

With all other factors or things remaining the same:

This means that we change one parameter at a time and watch how it influences the variables

For example: if the government cuts income taxes in order to lead to an increase in personal income, we would like to see whether consumption rises

If we hold everything else constant, we expect that most people will spend more money when their income rises

However, if at the same time there was a jump in prices and interest rates, people might not spend more money

This is why it is so important to isolate one change from another

In real life, of course, that is usually not possible and we have to make adjustments

Factors of production (FoP)

Basic components or inputs which are required in the production of goods and services

Land: Gifts of nature, this includes everything on the land, under the land, above the land, or in the sea (e.g., oil, water)

Labour: The human component hired to assist in producing a good or service

Simply the number of hours of work put in by a person

Capital: Any man-made aid to production

It is physical plant, machinery, equipment and buildings; it is not the money that you invest in the stock market

Entrepreneurship: Combines the other factors and takes risks recognizing the possibility of gain from employing these factors in a specific way

An entrepreneur is the one who sees an economic opportunity and mixes land, labor and capital together to produce a product with economic value

It is estimated that 85% of small businesses go bankrupt during the first five years; and 85% of those that survive go bankrupt in the next five years

There is a great scarcity of good management talent in the world

Factors of Payment:

Land: rent

Labour: wages (costs associated with using labour and are usually paid on an hourly/salary/commission basis)

Capital: interest

Profit: this is the return on investment in capital equipment:

We assume investments in capital equipment earn the opportunity cost rate of return (OCRR) in the market

Anything earned in excess of the OCRR is referred to as abnormal or super-normal profit or pure profit or economic profit

Abnormal profit: the amount earned in excess of normal profit and is calculated as the difference between what you receive for selling a good or service and the cost of producing it, including the effort you had to put into it and the OCRR you could expect to earn on the money invested in capital equipment

We refer to the amount received as total revenue, and the costs as total costs. Thus profit is equal to total revenue minus total cost

Most firms maximize profits by trying to increase revenues through better marketing, and decreasing costs through more efficient systems of production

If firms do not maximize profits, they will either not grow anymore because there are no profits to re-invest in the business, or they will be bought out by someone else who will then force the firm to maximize profit

Entrepreneurship: profit

Natural resources include all the resources we use such as land, trees, water, minerals

In Europe, rent is the income paid on natural resources such as land

In North America, rent is what is paid to rent an apartment and payments for using natural resources are called natural resource costs or raw material costs

There is some controversy about how to include environmental resources such as clean air, clean water, quietness etc.

When these are polluted there is a cost, how should that be included, and who should pay for it?

Economic Sectors

The primary sector involves the extraction of resources: farming, fishing, forestry and mining

The secondary sector involves the conversion of natural resources into goods: manufacturing and construction

The tertiary sector involves the production of services: finance and tourism

The quaternary sector involves production of technology, information services, education

In the private sector resources are owned by private individuals

Consumers are grouped into households which own the resources and decide what to buy and in what quantities

Rather than specialize on their own, most people sell their labour services to a firm and receive money wages in return

They also sell the services of other factors to firms in return for income

Producers expect to cover their costs with the revenue they obtain from selling:

Profit maximisation is essential otherwise the firm falls behind or is bought up by another firm which will force the first firm to maximize profits

Firms are the principle users of factors of production, they account for 85% of employment in most Industrialized countries

In the public sector production is in public hands: owned and controlled by the state which both buys and produces goods and services

We cannot assume that govts. always act in a consistent manner

Various governments make laws, the courts interpret these laws and uphold them

Any government measures that impose large costs with few obvious benefits to the current generation are unlikely to be popular:

Long run benefits are sometimes ignored: the planting of trees will only be enjoyed by future generations which do not have a vote today, therefore govt. will not spend money on planting trees

There is uncertainty about the future: it is hard to make decisions today which may have long term consequences

The satisfaction gained from the consumption of a good or service

Most people are assumed to be motivated by rational desires

Most people derive enjoyment or utility from the goods and services they consume, and most understand that the first amount of enjoyment from consuming a good is often the highest

As more and more is consumed, the level of enjoyment starts to decrease

This is referred to as the concept of diminishing marginal utility

The demand curve slopes downward because of the law of diminishing marginal utility (extra happiness)

The marginal utility is the enjoyment received from the next unit of whatever is being consumed, and it diminishes as more is consumed

Most people try to maximize total utility or enjoyment by consuming more than one good: as the marginal utility from consuming one good starts to fall from consuming more, you switch to another good where the marginal utility is higher (e.g., we do not just eat one food such as hamburger, we get more enjoyment from mixing it with other foods such as salad, potatoes and vegetables)

The marginal utility gained from buying an extra ice cream decreases with every ice cream we buy at a fixed price

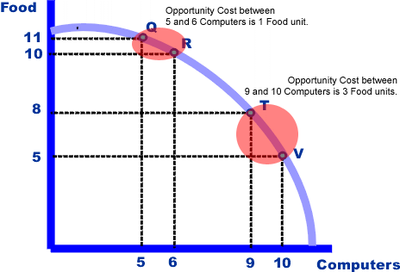

Opportunity cost

The cost of the next best alternative forgone

The cost of using a resource measured in terms of the sacrifice foregone in the next best alternative

When the best alternative is chosen from a range of alternatives the second best choice is the opportunity cost

If I have $5.00 and can either buy a tamogotchi or dinner, and I buy the tamogotchi, then the opportunity cost is the dinner I could have bought

Defined in terms of the THING that is forgone (i.e., not the monetary value)

Production Possibility Frontier (PPF)

A curve depicting all maximum output possibilities for two or more goods given a set of inputs (resources, labor, etc.). The PPF assumes that all inputs are used efficiently.

Free Goods

A good with no scarcity, that has unlimited supply and therefore no price

Free goods involve no opportunity cost such as fresh air, but they become economic goods if opportunity costs are involved in such things as removing pollution from the air

A good which has no opportunity cost associated with its consumption

Economic goods

A good which is scarce and therefore has a possible opportunity cost

Consumption goods are purchased by consumers and consist of perishable goods such as fresh food, semi-durable goods such as clothing, and durable goods such as cars

Capital goods are also referred to as producer goods are simply capital used in the production of consumer goods

Specialisation

Populations were fairly limited until the agricultural revolution and hunter gatherers were forced to do everything for themselves

Once agriculture developed people were able to specialize in the things they were best at doing, productivity increased dramatically

This created a surplus which could be traded for goods produced by people who had specialized in other areas

Trade

Trading occurred in markets where people could buy things more cheaply than they could make them

Originally, goods were traded through barter, but this required a simultaneity of desire: you had to find someone who had what you wanted and at the same time they had to want what you had to offer

Time was wasted trying to find satisfactory exchanges, and money was invented which eliminated the inconvenience of barter.

This release of wasted time led to a further increase in the surplus

Industrialisation

The industrial revolution introduced machinery allowing further specialisation:

Division of labour: workers specialized at tasks increasing productivity

Economies of scale: gains from bulk buying, large scale financing, and the use of large scale machinery permitted even further gains in productivity

We moved from labour intense production which uses relatively large amounts of labour compared to other factors, to capital intense production where relatively large amounts of capital are used compared to other factors

Resequencing: there are many ways to fabricate the parts for a product, and many different ways of assembling it

By altering the sequence of actions, a firm can find the most efficient way to fabricate parts and assemble them into a final product creating further gains in productivity and reductions in cost